Search our website enhanced by Google.

Tuesday, 30 April 2024

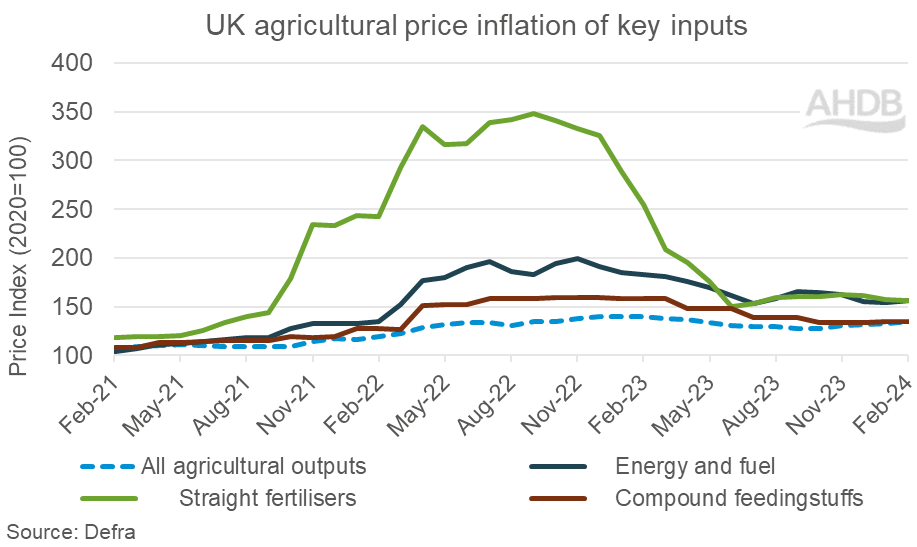

In February, the index for all agricultural outputs rose 1.5% month on month, and up 2.5% since the end of 2023. Strong growth in prices for key outputs such as sheep, cattle and potatoes have supped this inflation growth as tight supplies have been met with good demand. Year on year, the price index for all agricultural products has fallen as pricing for other key commodities such as milk and wheat have seen significant decline.

Straight fertiliser is the key input that has seen the most volatility in recent years, reacting to the natural gas markets. However, coming into 2024 it is the input that is consistently seeing a lower inflation index, with February down both on the month and the year. Prices for UK imported AN have fallen nearly £200/t over the last 12 months with prices in February 2023 averaging at nearly £538/t but at £347/t in 2024. As a net importer of fertiliser UK prices are more exposed to global market movements and it is likely prices will remain elevated from historic averages due to structural changes in the availability of domestic supplies.

Energy and fuel have seen a seasonal increase with the price index gaining 1.5% month on month in February as the northern hemisphere winter season provides an uplift in energy demand. Year on year the index has fallen 14.6% as wholesale gas and oil markets have eased as supplies increased, balancing with demand. However, continued poor weather has kept energy demand elevated at a time when we would typically begin to see it easing. Adding further pressure to the market is the ongoing geopolitical issues in the Middle East causing difficulties in the Red Sea trading route. These factors are likely to continue to influence prices in the coming months. Fuel prices have already seen growth in 2024, on the back of higher crude oil prices with red diesel prices averaging 85.3ppl in March.

Compound feed has seen minimal change in recent months, moving up only 0.2% month on month in February and 0.5% compared to the end of 2023. After the global market shock in 2022 caused by the outbreak of war in Ukraine, feed ingredient prices have been steadily declining resulting in the price index seeing a 15.0% decline year on year. Lower feed prices have helped to improve livestock farmers net margins, particularly in the pig and poultry industries where feed costs make up the largest share of producers cost of production. However, as with energy and fuel the continued wet weather is a cause for concern, with domestic plantings down and many farmers still struggling to access land with machinery to complete groundwork and spraying operations, this could lead to smaller yields. Global forecasts point to a tightness in the market this season with global supply and demand finely balanced, adding support to prices. The UK is likely to be more reliant on imported ingredients, exposing farmers to greater volatility.

Although wider economic factors such as interest rates, consumer price index and overall food inflation are easing or forecasted to ease this year, prices for most commodities are likely to remain at elevated levels, a potential new normal after the unrest of the last few years. As the UK becomes more reliant on imports, unfavourable weather conditions and trade disruption from conflicts are likely to result in continued market volatility in 2024. Hopefully this will be more subdued than recent years, allowing industry to regain confidence.

Subscribe to receive pork market news straight to your inbox. Simply complete our online form.

While AHDB seeks to ensure that the information contained on this webpage is accurate at the time of publication, no warranty is given in respect of the information and data provided. You are responsible for how you use the information. To the maximum extent permitted by law, AHDB accepts no liability for loss, damage or injury howsoever caused or suffered (including that caused by negligence) directly or indirectly in relation to the information or data provided in this publication.

All intellectual property rights in the information and data on this webpage belong to or are licensed by AHDB. You are authorised to use such information for your internal business purposes only and you must not provide this information to any other third parties, including further publication of the information, or for commercial gain in any way whatsoever without the prior written permission of AHDB for each third party disclosure, publication or commercial arrangement. For more information, please see our Terms of Use and Privacy Notice or contact the Director of Corporate Affairs at info@ahdb.org.uk © Agriculture and Horticulture Development Board. All rights reserved.

Topics:

Sectors:

Tags: